Part II: Loch Ness Monster, Indirect Costs, and other folklore.

Unlike indirect costs, there is no real proof that the Loch Ness Monster exists despite the many sightings since ancient times. In recent years all the alleged pictures have been debunked and people claiming to have seen her have been outed as charlatans. The famed Nessie photo that we have all seen, was taken in 1934 and is known as the ‘surgeon photograph’. Only recently it was proven to be fake and was a photo of a head and neck cutout attached to a toy submarine. Below we will look at the very real but mysterious process of indirect cost negotiation and what those costs cover.

To ease administrative burden and to harmonize processes across sponsors, universities now negotiate indirect cost rates with one of two main cognizant agencies: the ONR or the DHHS. According to the federal regulations governing federal grants and contracts to universities, Uniform Guidance, our Federal Sponsors must accept those rates. As part of that negotiation, CSU provides our cognizant agency DHHS – Cost Allocation Services, financial statements showing the costs that have been expended for the various Activity Types on campus: Sponsored Research, Instruction, Other Sponsored Activities, or Other Institutional Activities. Along with the financials, we provide a space survey. For departments deemed to be “high research,” the survey shows how individual rooms in their buildings are used for the activities above. The spaces in other departments are assumed based on the department and room type. The information provided allows CSU and DHHS to negotiate a rate for each activity type based on actual costs.

The negotiated rate though is never as high as a calculated actual rate for many reasons.

- For ease of administration (and to reduce administrative costs) CSU negotiates pre-determined rates with our cognizant agency. Since these rates are fixed, we may not get reimbursed in full for previously expended support of sponsored activities. These activities include having the facilities, administrative support, and internal controls needed to submit a proposal and compliantly administer a Federal award regardless of whether it is funded. While it will vary by sponsor and discipline, hit rates on awarded proposals remain low, according to a Google search, somewhere between 10% – 30% of proposals submitted.

- There are restrictions on indirect cost rates imposed by statute or appropriations bill language*.

- The “A” (administrative) component of the F&A rate has been capped at 26% for the last 30+ years, even as administrative requirements and resulting costs have steadily increased.

- *DYK – There are certain programs where funds have been appropriated by Congress with specific requirements including the mandated use of a lower indirect cost rate, such as the USDA Farm Bill and the Department of Education restricted rate programs. These are exceptions, not the norm, and result in Universities subsidizing Federal research.It should be noted that indirect cost rates for industry research entities are often much higher than their university counterparts.

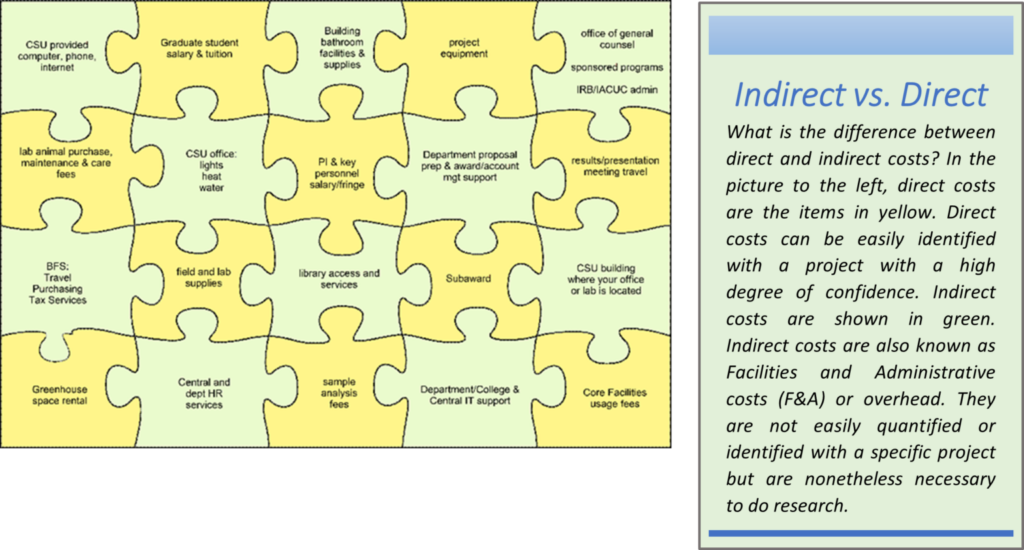

Indirect costs are actual incurred costs for supporting sponsored projects (research and public service) on our campus. They are hard to quantify on each project due to many projects using the same resources in possibly small amounts, which is why they are expressed on a budget as the negotiated percentage. The dollars that we receive for indirect costs go to pay for buildings and labs; facility maintenance; utilities; libraries; central and departmental administration; and student services that are used in research. Both direct costs AND indirect costs fund sponsored activities.

Why Do I Care? Research is expensive. To continue being able to conduct vital research at universities, we must include the full, allowed indirect cost rate in all proposal budgets to recoup as many of the actual costs of doing business as possible. Because, unlike Scotland which is laughing all the way to the bank on the windfall tourist dollars it receives each year from the Loch Ness Monster, universities are struggling to support their research enterprise in an environment where compliance and oversight are increasingly being mandated by our sponsors.

If you would like to investigate the history and current culture of indirect costs or the Loch Ness monster, here are the resources used for this blog.

- NSF.gov, Federally Sponsored Research: How Indirect Costs are Charged by Educational and Other Research Institutions, https://www.nsf.gov/pubs/1997/oig912/oig912.pdf

- NIH Extramural NEXUS, All About Indirect Costs, Sally Rockey, 9/11/2015, https://nexus.od.nih.gov/all/2015/09/11/all-about-indirect-costs/

- AIP.org, CRS Report: History of Indirect Cost Policies, https://ww2.aip.org/fyi/1994/crs-report-history-indirect- cost-policies

- Grants.gov https://www.grants.gov/learn-grants/grant-policies/omb-uniform-guidance-2014.html

- The Office of Scientific Research and Development (ORSD) Collection, https://www.loc.gov/rr/scitech/trs/trsosrd.html

- A Primer on Indirect Costs, University of Washington, March 1992, https://www.cogr.edu/sites/default/files/SKM_C36818013111170.pdf

- The Heritage Foundation, Indirect Costs: How Taxpayers Subsidize University Nonsense, Jay Greene, Ph.D, and John Schoof, 1/18/2022, https://www.heritage.org/education/report/indirect-costs-how-taxpayers-subsidize- university-nonsense

- CSU Morgan Library search: https://lib.colostate.edu/search-website/

- Loch Ness monster, Britannica, August 26, 2023, Amy Tikkanen

Additional resources:

- Preparing Budgets on Sponsored Projects, OSP Guidance webpage

- Indirect Costs Extend Beyond Sponsored Research, December 19, 2018, Tricia Callahan

- Understanding Indirect Costs One Pickle at a Time, May 21, 2020, Tricia Callahan

Blog post by Shannon Irey, OSP Training and Information Coordinator, with contributions from Chris Carsten, OSP eRA Systems Officer, Bill Moseley, OSP Pre-Award Manager, Jacque Clark, BFS Manager – Cost Analysis, Property Management & Banner Admin, and Doug Leavell, OVPR Director Research Analytics.